Reward programs are incentives designed to create loyalty among customers and to provide the best rewards to the "best" customers.

These programs have proliferated in the hospitality industry for nearly three decades, with little direct evidence that they actually build either attitudinal or behavioral loyalty.

While program implementation seems to have expanded exponentially, the actual components and structure of any given program appears to be driven more by what the competition is offering rather than demonstrated effectiveness.

This report by Cornell (1) identifies program components that have been shown to be effective, and (2) offers a series of guiding principles that hospitality and marketing managers should find useful in designing and modifying their reward programs.

When Hilton Hotels decided to raise the number of loyalty points required for a free hotel stay earlier this year, IHG pounced.

They launched a campaign for their Priority Club rewards program that called out the changes to the Hhonors frequent guest program via a contest called the "Luckiest Loser".

The consumer who was the "luckiest loser"--the one with the most points invested in the HHonors program--won 2 million Priority Club points.

Additionally, 20,000 "lucky losers" got up to 20% of their current HHonors balance in Priority Club points. Everyone else got 1,000 points just for entering.

Does this make long term sense according to the Cornell report, I wonder? It seems to make a lot of good short term sense.

Since February, 2010, there has been a spate of chain

restaurant merger and acquisition action underway: CKR (Carl's/Hardees's), Papa

Murphy's,Rubio's , On the Border, Lubys

buying Fuddruckers, just announced today, via Chapter 11 auction

results, for $60M); and rumored , Nelson Peltz selling Wendy's/Arby's. Some of the prices paid have been pretty low

(CKR) and some much higher.

This was all somewhat predictable. And all of these transactions involve franchisees, in the mix.

In some cases, private equity (PE) firms are eager to

rebalance their portfolios and sell their concepts outright, or to buy the

chains for later turnaround/later initial public offering (IPO). And Denny' recently had the battle royale of

proxy contests, where an outside, dissident force hoping to get board seats was

narrowly turned back.

How the debt is done, what the leverage and interest costs are

what the plans for management, supply chain and future business expansion matters to franchisees.

For most of these chains, about 80% of the stores are

franchised, and the franchisee owners

collectively have more money invested in the current total enterprise value

than does the company.

Just today, I saw a prominent restaurant security analyst's report

that valued franchise earnings (company franchise operational profit, the

royalty stream) at twice the multiplier rate of company owned stores...wow...that's

a lot of money for that fairly predictable piece of the top line that the

franchisor receives in royalties.

Of course, associations aren't consulted nor have much

information about this. The company views the buyout deal as complicated enough

without involving franchisees.

Here are some suggestions for franchise associations:

(1)Buy

some company stock. That elevates the franchisee associations a bit, and gives

access to stockholder meetings, and other communications.

(2)Monitor

the news, and include articles in your newsletters. Both the International Association

of Franchisees and Dealers www.franchise-info.ca and www.bluemaumau.org have daily news

clips and columns touching on these topics.

(3)Document

and come to agreement on your business strengths and weaknesses. And how to

respond. You may need this information someday.

John A. Gordon is a restaurant

financial analyst and management consultant, and can be reached via (619)

379-5561, or [email protected].

Payroll cards, a less costly alternative to paper payroll checks, allow employees to access their pay through various means, depending on the particular product.

Wages are deposited to the payroll card account via direct deposit, and the employee uses the card to withdraw cash at an ATM or purchase goods and services.

One of the distinguishing characteristics about bank-issued payroll cards is that they generally are not marketed directly to consumers.

Instead, banks market the cards to employers, who, in turn, encourage their employees who do not use direct deposit to use a payroll card to receive their wages.

The payroll card is a particular type of stored value (or prepaid) card, a product that streamlines the payment process for purchases or cash withdrawals. A variety of stored value cards exist, including prepaid phone cards, mass transit cards, and prepaid debit cards.

Stored value cards operate in either "closed loop" or "open loop" systems. In the closed loop system, an issuer provides a card that can be used only for its products or at a finite number of merchant locations.

Mass transit fare cards and college-issued cards that can be used at cafeterias, bookstores, and other campus venues typically have closed-loop systems. In an "open loop" system, cards are accepted beyond the issuer's locations through a more universal network for PIN-based (e.g., STAR) or signature-based (e.g., Visa, MasterCard) transactions.

Payroll cards use an open loop system, and should probably find there way into most franchisee operator's payroll tools.

Few employers believe that the new health reform law will address their Number 1 concern -- controlling

health care costs -- according to a new survey by Towers Watson.

When asked about the health care goals that are most important to their organizations, 96% of respondents

identified cost containment as an essential or high priority; 88% pointed to encouraging healthier lifestyles;

and 75% identified improving the quality of care.

When they look at the Patient Protection and Affordable

Care Act, however, nearly all respondents (94%) believe that the law will raise their costs; 61% believe it

will have a minimal effect on encouraging healthier lifestyles, and 73% believe it will have either a

negative impact on the quality of care or none at all.

"While many employers have not yet assessed the full impact that reform will have on their businesses,

they do realize that the responsibility to hold costs down will fall primarily on their shoulders," said Mark

Maselli, North American Health and Group Benefits Leader for Towers Watson.

In order to cope with anticipated cost increases, many employers plan on:

Employers remain committed to pre-PPACA initiatives designed to hold the line on rising medical costs

and improve employee health. For example, only 12% said they would eliminate or reduce their

wellness/health promotion programs in the wake of health care reform.

In fact, 48% of survey respondents

believe that the law will result in an overall increase in the number of wellness programs.

In addition, employers expect that PPACA will lead to increases in:

� Adoption of total replacement consumer-directed health plans (58%)

� Transparency of provider prices (37%)

� Provider quality (35%)

(The online survey, conducted in May 2010, drew responses from 661 large firms.)

"You don't want the government to come calling and decide you owe a lot of back taxes for classifying contractors incorrectly.

Be vigilant about reading the government's contractor classification guidelines and make sure your contractors actually fall within them."

The trade-offs and problems of contingent workers are nicely summarized by Steve King, at Small Business Labs.

"Federal and state governments claim they lose billions of dollars in payroll taxes due to under-reporting by contractors.

They also claim they collect less in unemployment insurance and worker compensation taxes. Because of this, they are aggressively going after companies they feel mis-classify full time employees as contingent workers.

This issue has huge implications because: (1) companies of all sizes are increasing their use of contract workers; and (2) a growing number of people are choosing to work as independent contractors.

This used to be much simpler issue from the standpoint of the contingent worker - they almost always wanted to become full-time employees.

But that has changed.

A growing number of people are seeking the flexibility and work/life balance advantages contract work brings."

The Employee Misclassification Protection Act of 2010 (EMPA), amends the federal Fair Labor Standards Act (FLSA) to Increase government enforcement against employee misclassification practices by employers of all sizes, to curtail and penalize worker misclassification.

EMPA sets strict notice and record-keeping requirements on all employers, with costly penalties for non-compliance (up to $5000 per worker).

It requires all states to develop and enforce their own employee misclassification enforcement programs through audits and other methods.

"The most important trends of the last few decades is the growing use of contingent workers. This is a structural shift towards employer use of contractors, freelancers, part-timers, etc. instead of hiring full-time, permanent employees."

For more information, King says that "Staffing Industry Analysts are the leading, and maybe the only dedicated) analysts in this space.

Their site, blogs and magazine also has lists, ads and references to firms that do contingent workforce compliance.

In addition to Industry Staffing Associates, Workforce Week is another good source on services related to the contingent workforce. It has broader HR related coverage, but it seems like they usually have an article or two on contingent workers each week."

The franchisor is obligated to give a prospective franchisee financial disclosure of the franchisor's business.

One of my concerns is that this financial disclosure is less than what a shareholder gets in a public company.

A shareholder can exist relatively quickly, but a franchisee is usually stuck for the term of the franchise contract - a situation that calls for more disclosure and not less.

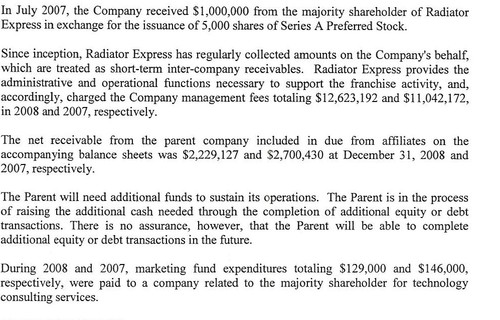

Here is the type of example that should be of concern, from the franchisor 1-800 Radiator's 2009 filing.

A number of questions spring to mind, especially since this is buried in the footnote of the financials.

1. Is Radiator Express really the franchisor, if it is doing all the collection and operational functions? If so, where are its financials - it being the "parent company"?

2. How much additional funds does the Parent need? Is it in danger of no longer being an going concern? What will happen to the franchisee operational support being provided?

3. It is now the middle of 2010 and there has been nothing filed on Caleasi which answers question 1 or 2. Is Radiator Express insolvent, preparing a receivership, or preparing for bankruptcy. Franchisees really need to know this.

4. Radiator Express, in this note, appears to be charging the franchisor a sum equal to most of the franchisor's revenue. But where is the explanation of what forms the basis of these charges - we don't have any information in the FDD about Radiator Express.

I could be way off base on this questions, and maybe there is a simple answer. Does anyone from 1-800 Radiator have an explanation?

"Location, Location, Location" is the oft-repeated mantra meant to emphasize the importance of the right site to the success of any retail business.

But what are the key factors for you to understand with regards to your location choice?

The three most important real estate-related drivers for any type of retail business are:

(1) the size and quality of the trade area served;

(2) number and quality of your competition and;

(3) the type of shopping center and other site-related qualities.

A common mistake is to ignore the distinction between a trade area and a site within that trade area. A trade area is the market area that will be served by your business. The trade area has geographic boundaries and consists of a mix of uses (home, work, shopping, entertainment and public facilities).

Tip: a good mix of uses tends to provide higher sales potential mainly because there's activity in the trade area for most of the day and 7 days a week. The demographic profile of the residents of the trade area is critical, too.

The demographic profile should match your customer profile (if you're a franchisee, your franchisor should tell you the target customer profile in detail). A large population base is good only if there are a lot of your customers.

The precise size of a trade area is determined by community affiliation, travel and shopping patterns, and natural and man-made barriers.

Think of the difference between the trade area and your site in this way: the trade area is the market area you hope to tap, and your site is the location in that trade area that will determine how much of that trade area you'll reasonably be able to serve.

Your type of business and the location of competitors are key elements that determine your reach into the trade area.

For example, a dry cleaner is largely a convenience business, and there tends to be a lot of competitors. Unless you offer particularly unique services or your competitors are poor operators, you'll be cut off by other similar businesses that are more convenient to customers in the trade area. You should seek to "out-position" your competition, so pick a site that's defensible, both now and in the future.

Your trade area reach is also determined by the type and location of the shopping center your chose (neighborhood, community, power center) as well as the center's site characteristics (such as sufficient parking, ease of access and signage).

A traditional grocery store in a suburban area tends to pull 2-3 miles, and the other tenants in those centers tend to be convenience tenants that also have limited reach.

If there are tenants that have a larger draw, such as specialty grocers or other "big box" tenants, you'll have the opportunity to draw from 5 miles or more into the trade area. That's why it's important to locate with co-tenants that will serve as generators for your business.

All things equal, you'll want to be in a strong shopping center with co-tenants that provide generators for your business. But remember that no matter how strong the shopping center and your space within that center may be, you will always have an uphill battle if you're "fighting the market".

I've seen stores with even poor site characteristics do strong sales, and this was largely attributable to the strength of the trade area for that tenant.

Make sure you'll be serving the right trade area before focusing on any specific site. A strong location in the right trade area makes a winning combination.

A study entitled "2009 Forbes/CIT Survey" completed last fall included the following retail statistics:

- 40% of tenants had renegotiated their rent - 38% negotiated other types of concessions - 28% received Landlord allowances on new leases - 22% had reduced their overall occupancy expenses.

It's no secret that rents are down (anywhere from 20-40% depending on your location) and that corporate, multi-unit tenants have real clout and are using the condition of the great recession to ratchet down their rents.

But how does the small business operator take advantage, even in the short term? (The current consensus is that retail rents will remain depressed in most areas through 2011, due to an overabundance of vacant, retail space and the forecasted modest demand in the short term.)

Here are (4) actionable tips for good operator to reduce their retail occupancy cost.

Franchisees who have a good track record with their Landlord have an opportunity to reduce their overall occupancy costs and this can be accomplished in a number of ways. If your operations and sales performance are historically strong, a Landlord will have every motivation to work with you because right now he is limited in his ability to replace you.

First, read your existing lease for any conditions that the Landlord may be violating, such as co-tenancy provisions or vacancy levels. For example, the Landlord might have agreed to have a certain anchor tenant and that tenant is no longer operating. Or he might be in violation of a maintenance standard provision. If you find anything in your lease that is a violation or a potential default by the Landlord, this gives you additional leverage in your negotiations.

Second, annual base rent is an obvious target for modification. You need to do your research by finding out the asking rents in competing centers. Also learn what the Landlord is currently asking for vacant space in your center. If your lease commenced after 2004, chances are your rent is significantly above-market. The Landlord could agree to temporary "rent relief", which is generally a short-term reduction (a year or two) but might expect to recoup that reduction later on. If you agree to a payback, tie it to a sales threshold. This is a win-win for both you and the Landlord.

Third, occupancy cost isn't just rent. In some centers, Common Area Maintenance (CAM) charges are high. Part of your negotiations, if you don't have this already, is to "cap" the CAM charges, which is standard practice for corporate-owned businesses. Also, make sure your lease reads that your pro-rata share of the CAM (as well real estate taxes and insurance on the center that are passed through to tenants in most retail situations) is based on your total square footage divided by the total square footage of leasable space in the center (not "leased" space). The Landlord should be paying CAM on vacant spaces. If your lease doesn't read that way, change it as part of your rent renegotiations. This is a quick way to reduce your occupancy cost.

Fourth, another part of your occupancy cost is a marketing association charge for the shopping center (for example, $1 a square foot). Ask the Landlord to show you how those marketing dollars are being spent and if it's not helping you, try to get this charge omitted from your lease, or at least reduced. Another expense is the administrative fee percentage that's usually noted in the CAM section of your lease. Anything over 5% is too much.

If you hope to stay in your existing location for the foreseeable future, or there's a better space in the same shopping center that's opened up, consider negotiating an extended term or a new lease. This is valuable to you if you get what you need in that lease, and the Landlord benefits in that he'll have a more bankable lease on your space.

It's worth the time and effort to reduce your occupancy costs. Most of these costs are fixed. If you lower them now you'll be better positioned to survive the current market and you'll be more profitable as your sales increase in the future.

what Washington is saying to th public, and what is

happening on the ground regarding small business loans.

"The bank examination climate today is perhaps the most severe in two generations at least," says Cam Fine, CEO of Independent Community Bankers of America (ICBA).

"It's like a reign of terror, particularly on the community banks," which serve a disproportionate number of small firms.

In public statements and interviews, regulators say they've repeatedly told their examiners to encourage banks to lend to creditworthy borrowers.

Examiners, they say, are generally fair, affording bankers ample leeway to make their own judgments.

Yet, officials acknowledge that examiners are more vigilant in light of the lax credit standards that triggered steep downturns in housing and commercial real estate and a continuing rise in the number of loan defaults and bank failures. Since early 2009, 177 banks have shut down, and more than 700 are on the FDIC's "problem bank" list.

Commercial real estate -- which makes up nearly a third of community banks' loan portfolios -- continues to be plagued by rising vacancies and plummeting value.

Still, officials concede, examiners may go too far sometimes.

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_e.png?x-id=0ca09967-726b-4fb3-a54c-6288c849990e)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_e.png?x-id=82cd0b6e-1385-426b-9cd2-73152a1413ae)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_e.png?x-id=076ad5ec-4059-4a41-a6b1-055653516330)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_e.png?x-id=e38b56a2-7233-4fd4-a59d-a14ea6ec2370)